### Date : 2024-09-09 16:08

### Topic : Wage Determination and Labor Market Equilibriums #macroeconomics #economics

----

## 14.2 Wage Determination and Labor Market Equilibrium

**Introduction:**

Wage determination is a critical aspect of labor economics and refers to how wages are set in the labor market. Labor market equilibrium occurs when the quantity of labor supplied by workers equals the quantity of labor demanded by employers. In this equilibrium, the wage rate is determined by the interaction of supply and demand forces.

### Definitions:

1. **Labor Supply (Workers):**

- **Definition:** Labor supply refers to the total hours that workers are willing and able to offer at a given wage rate in the labor market. It is determined by factors such as wages, working conditions, individual preferences, and the availability of alternative employment opportunities.

- **Example:** If wages increase, more people may be willing to enter the labor market, increasing the supply of labor.

- **Sources:** Borjas, George J. _Labor Economics_, International Labour Organization (ILO).

2. **Labor Demand (Employers):**

- **Definition:** Labor demand refers to the number of workers employers are willing to hire at various wage rates. It is a derived demand, meaning it depends on the demand for the goods and services that labor helps produce. Employers hire more labor if the wages are lower and the marginal productivity of workers is high.

- **Example:** A factory hiring more workers because of higher demand for its products.

- **Sources:** Borjas, George J. _Labor Economics_, World Bank.

3. **Bargaining Power:**

- **Definition:** Bargaining power is the relative ability of workers (employees) or employers to influence the terms and conditions of employment, such as wages and working conditions. Workers may have more bargaining power through unions, while employers may have more power when labor supply exceeds demand.

- **Example:** In industries with strong unions, workers have greater bargaining power to negotiate higher wages.

- **Sources:** International Labour Organization (ILO), _The Economic Journal_.

4. **Productivity:**

- **Definition:** Productivity refers to the efficiency with which labor can convert inputs (like time and effort) into outputs (goods or services). Higher productivity generally means more output is produced per hour of work, which can lead to higher wages for workers.

- **Example:** A worker in a high-tech industry who can produce more goods per hour than a worker in a low-tech industry.

- **Sources:** OECD, _Productivity in the Global Economy_.

5. **External Market Conditions:**

- **Definition:** External market conditions include factors outside the control of individual employers or workers that influence the labor market. These include economic growth rates, inflation, global trade dynamics, technological changes, and government policies.

- **Example:** A recession leading to lower demand for labor as businesses cut costs.

- **Sources:** _Journal of Labor Economics_, World Bank, OECD.

### 1. Wage Determination

Wages in an economy are determined by a variety of factors, including the interplay between labor supply (workers) and labor demand (employers), bargaining power, productivity, and external market conditions.

#### Factors Influencing Wage Determination

1. **Supply and Demand for Labor:**

- **Labor Supply:** The labor supply curve shows the relationship between wages and the quantity of labor workers are willing to supply. As wages increase, more workers are willing to enter the labor market, so the supply curve typically slopes upward.

- **Labor Demand:** The demand for labor is a derived demand, meaning it depends on the demand for the goods and services that labor helps produce. Employers will hire workers as long as the revenue generated by an additional worker (the marginal revenue product, MRP) is greater than or equal to the wage. As wages increase, the quantity of labor demanded decreases, so the labor demand curve slopes downward.

2. **Marginal Productivity of Labor:**

- Wages are influenced by the productivity of workers. According to the **Marginal Productivity Theory of Wages**, employers pay workers based on their productivity (how much additional output they produce). More productive workers, or those in sectors with high output prices, tend to receive higher wages.

3. **Bargaining Power and Institutions:**

- **Unions:** In industries where unions are present, collective bargaining can lead to higher wages for workers. Unions negotiate with employers on behalf of workers to secure better pay and working conditions.

- **Minimum Wage Laws:** Governments may set minimum wage laws that create a wage floor, ensuring that no worker earns below a certain amount. This can lead to wage levels higher than the market equilibrium in some sectors.

4. **Human Capital:**

- Workers with higher levels of education, skills, and experience (human capital) tend to command higher wages. The more specialized or in-demand a skill set is, the higher the wage rate for those possessing such qualifications.

5. **Market Power and Discrimination:**

- Wage determination can also be affected by **monopsony power** in the labor market, where a single or few employers dominate the hiring market, which can suppress wages.

- **Discrimination** based on gender, race, or other factors can lead to wage disparities that are not related to productivity or job type.

### 2. Labor Market Equilibrium

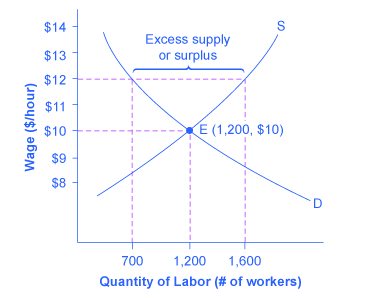

**Labor Market Equilibrium** occurs at the point where the labor supply equals labor demand. At this point, the wage rate and the level of employment are stable, and there is no excess demand or supply of labor.

1. **Equilibrium Wage:**

- The equilibrium wage is the wage rate at which the quantity of labor demanded by employers equals the quantity of labor supplied by workers. This is determined by the intersection of the labor supply and labor demand curves.

- At the equilibrium wage, all workers who are willing to work at that wage can find employment, and all employers who are willing to hire at that wage can find workers.

2. **Labor Surplus (Unemployment):**

- When the wage is set above the equilibrium level (such as with a government-imposed minimum wage), a labor surplus occurs. This leads to unemployment because more workers are willing to work at the higher wage, but employers are not willing to hire as many workers at that cost.

3. **Labor Shortage:**

- Conversely, if wages are set below the equilibrium wage, a labor shortage occurs. Employers want to hire more workers at the lower wage, but fewer workers are willing to work at that wage level.

### 3. Shifts in Labor Market Equilibrium

Shifts in labor supply or labor demand can cause changes in the labor market equilibrium:

1. **Shifts in Labor Supply:**

- An increase in the supply of labor (e.g., due to population growth, higher immigration, or more people entering the workforce) shifts the labor supply curve to the right, potentially lowering wages.

- A decrease in labor supply (e.g., due to aging populations, emigration, or reduced workforce participation) shifts the supply curve to the left, raising wages.

2. **Shifts in Labor Demand:**

- An increase in labor demand (e.g., due to technological advancements, higher demand for goods and services, or economic growth) shifts the demand curve to the right, raising wages and employment.

- A decrease in labor demand (e.g., due to economic downturns, automation, or outsourcing) shifts the demand curve to the left, reducing wages and employment.

### 4. Role of Government Policies and Institutions

1. **Minimum Wage:**

- Setting a minimum wage above the equilibrium wage can cause labor market distortions, such as unemployment if employers are unwilling to hire at the higher wage. However, it can also lead to improved living standards for low-wage workers.

2. **Unemployment Benefits and Labor Market Regulations:**

- Unemployment benefits and labor market regulations can affect the willingness of individuals to work and the cost of hiring for businesses. Generous unemployment benefits might reduce labor supply, while strict labor regulations may increase the cost of labor for employers, shifting the labor demand curve.

3. **Taxation and Subsidies:**

- Payroll taxes can reduce take-home pay for workers and increase the cost of labor for employers, potentially reducing labor demand. Conversely, subsidies for hiring (e.g., tax credits for employers) can increase labor demand and employment.

### 5. Real-World Examples

- **Technological Change and Automation:** In industries like manufacturing, technological advancements have shifted labor demand. Automation reduces the need for low-skilled workers, leading to a shift in demand towards more highly-skilled workers, increasing wage disparities across skill levels.

- **Globalization and Outsourcing:** The outsourcing of jobs to countries with lower labor costs can reduce labor demand in higher-cost countries, leading to downward pressure on wages and employment in affected industries.

### Conclusion

Wage determination and labor market equilibrium are shaped by complex interactions between labor supply and demand, worker productivity, institutional factors like unions and minimum wage laws, and broader economic forces like globalization and technological change. Understanding these dynamics helps explain wage levels, employment rates, and the effects of policy interventions in the labor market.

### Reference:

-

### Connected Documents:

-