### 날짜 : 2024-03-25 13:12

### 주제 : Consumer Choice and Demand #economics

----

### 4.3 Consumer Choice and Demand

Consumer choice, underpinning demand in microeconomic theory, outlines how consumers utilize the income they have to purchase goods and services that provide them with the highest level of satisfaction or utility. We'll examine the connection between the consumer's choice and how it generates market demand curves for goods and services.

#### The Basic Model of Consumer Choice

The basic model of consumer choice brings together preferences (which can be represented by indifference curves), budget constraints, and the [[Optimization Rule]] (marginal rate of substitution equals the price ratio of two goods) to determine the best bundle of goods that a consumer can and will purchase.

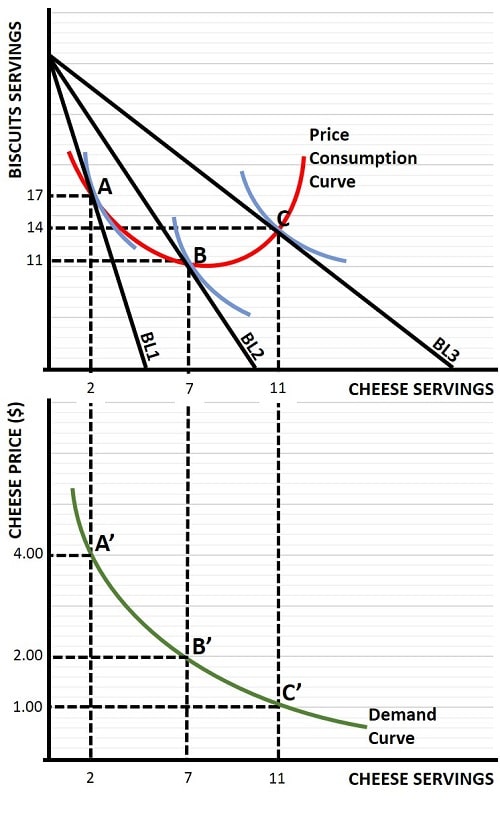

#### Deriving Demand from Consumer Choice

1. **Price Consumption Curve (PCC)**: If we change the price of one good and keep everything else constant, we trace out a price consumption curve that shows how the chosen consumption bundle changes as the price changes.

2. **Income Consumption Curve (ICC)**: Similar to PCC, an income consumption curve shows how the consumer's choice of goods changes as their income changes, holding prices constant.

3. **Individual Demand Curve**: By taking one good's PCC and noting the quantity demanded at different prices (while keeping the consumer's income and the prices of all other goods constant), we can trace an individual demand curve for that good.

#### Factors Influencing Consumer Choice and Demand

1. **Prices of Goods**: As the price of a good increases, consumers tend to purchase less of it (law of demand), assuming the good is a normal good.

2. **Income of Consumers**: Increases in consumers' income usually lead to increased demand for normal goods (goods for which demand increases when income increases).

3. **Tastes and Preferences**: Changes in consumer tastes can shift demand. For instance, if a health scare arises concerning a particular food item, demand for that item will probably decline.

4. **Expectations**: Anticipated changes in prices or income can affect the current demand for goods and services.

5. **Price of Related Goods**: Substitutes and complements influence demand as well. If the price of a substitute falls, demand for the good in question usually decreases. Conversely, an increase in the price of a complementary good typically lowers demand for the good in question.

#### Elasticity of Demand

Demand elasticity is a measure of how responsive the quantity demanded of a good is to changes in various factors such as the price of the good itself (price elasticity of demand), consumer incomes (income elasticity of demand), or the prices of related goods (cross-price elasticity of demand).

#### Example: Coffee Market

Consider the demand for coffee. Suppose that due to a new study extolling health benefits, consumer preferences shift towards more coffee consumption. This shift would move the individual demand curves to the right, indicating a higher quantity demanded at each price level. If this preference shift is widespread across consumers, the market demand for coffee would increase.

Now, imagine that the price of tea (a substitute for coffee) decreases. Some coffee drinkers might switch to tea, reducing the demand for coffee. This reaction would be represented by a movement along the demand curve for coffee (decrease in quantity demanded due to a change in the price of a substitute).

If consumers' incomes rise and coffee is a normal good, there would be an outward shift in the demand curve for coffee, meaning more coffee would be demanded at every price level (illustrating the income effect).

Lastly, consider price elasticity. If coffee has a high price elasticity of demand, a small increase in the price of coffee will cause a relatively large decrease in the quantity demanded. If coffee is an inelastic good (consumers need their morning fix, regardless of cost), then price increases may not lead to significant changes in quantity demanded.

#### Applying to Market Demand

The aggregation of individual consumer choices forms the market demand curve for a product. In a market, thousands or millions of consumers make individual choices based on their preferences and constraints. These choices, taken together, make up total market demand.

### Practice Application

A useful exercise to solidify understanding of these concepts is to work with hypothetical scenarios:

1. Analyze how a change in the price of a substitute (like tea for coffee) affects the demand for the original good.

2. Examine the effect of an advertising campaign on consumer preferences and how that might shift demand.

3. Consider introducing a new budget constraint, like a tax on luxury goods, and predict how this might shift individual and market demand curves for various goods.